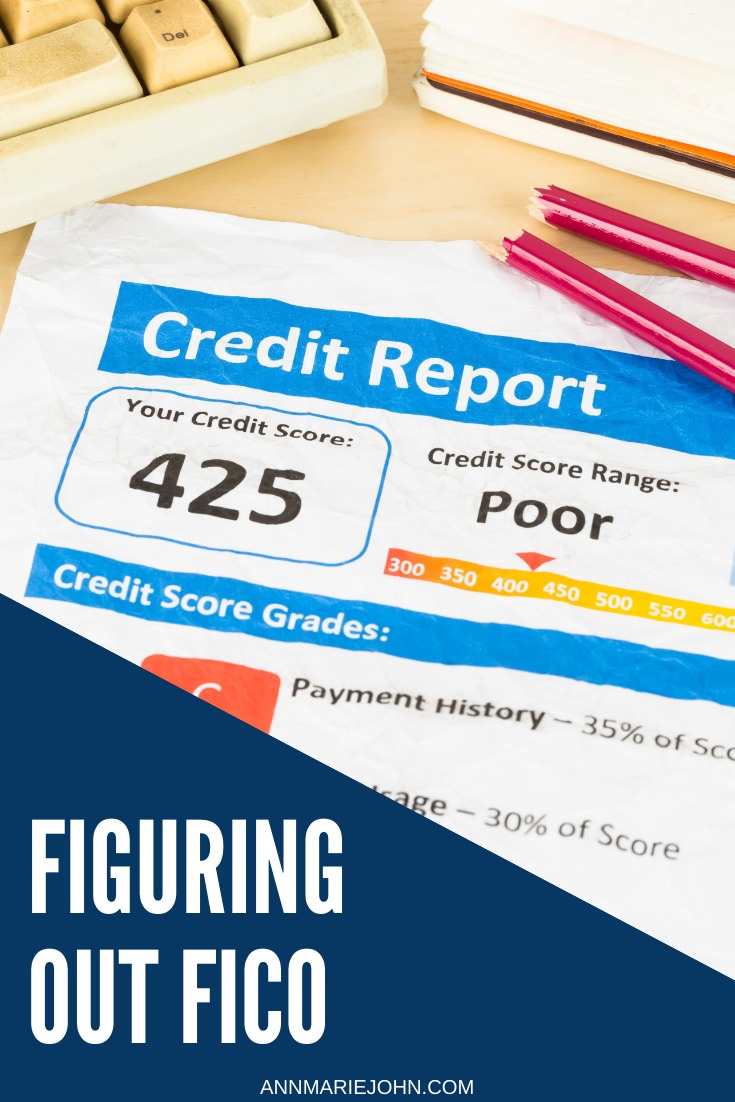

It would be hard to get through life working on an entirely cash-only system, although for some, that approach is successful. However, for large purchases such as a residence, an automobile or heavy machinery, you may need financial assistance to conduct your transaction. In order to evaluate your financial reputation, potential lenders check your credit score. This is a number that represents what a lender can expect with your creditworthiness and your financial habits.

A credit score can be taken from several different reporting agencies, although a FICO score tends to be the final number taken from these reports. Between Equifax and Experian there are 16 different scores that could be reported to a lender, and the other leading reporting company, TransUnion, has 21 different scores. It is said that there are more than 50 FICO scores that could be reported, and new score types are added each year. The past few years have seen some changes in the FICO scoring models, an adjustment that could create a FICO score update for your credit report.

INDUSTRY-SPECIFIC REPORTING AND SCORING

The type of loan or financing that is being requested influence what scores are reported. The industry-specific scores make it possible to obtain products like auto loans, credit cards, or furniture leasing. The information these credit reports provide is similar in nature to the classic scores FICO issues, but there are some tweaks made to account for potentially risky behavior that is industry-specific. For instance, if you are attempting to buy a car, the bank or dealership that may offer you the loan might want to know your history with paying similar loans over a course of time. They then factor in the other accounts of credit card payments, rent payments, or utility payments to assess what kind of risk your loan might be. The scoring models for these industry-specific scores are much different from classic scores, as the industry-specific range extends from 250 to 900. Classic scores only range between 300 and 850.

UNDERSTANDING THE SCORING MODELS

You won’t be able to calculate a credit score on your own, even though you may know the different areas that impact your score and what your standings in those categories are. Companies that have created the scoring models have kept the calculation algorithms under lock and key, because of the financial benefit they receive from selling the results of the models. There are five primary areas of calculation, and these include credit history, credit utilization, credit payments, credit accounts, and new credit applications. More specifically, the following factors are important contributors to your score.

- Missed payments, collections, bankruptcies, foreclosures

- Employment history and occupation

- Your residence situation (rent or own)

- Length of time at your current residence

- Credit inquiries over the last few months or years

- Balances available or used in open credit accounts

- Credit report length and credit history with the reporting agency

- Your age

SCORING MODEL UPDATES

The first credit scoring models came on the scene over 50 years ago. The financial industry was looking for a reliable but repeatable method of evaluating, underwriting, and administering credit debt. The need for financial evaluations included home mortgages, automobile loans, credit cards, or direct and indirect consumer installment loans. The earliest models were based on subjective criteria, and the end result was an increase in fraudulent credit and loan practices and approvals, as well as discriminatory decisions with borrower’s applications. Federal and state legislatures got involved, and protections were established to make the lending process more transparent, equitable, and fair. Two of the most well-known protections are the Equal Credit Opportunity Act and the Fair Credit Reporting Act.

THE BENEFITS OF USING A MODEL

Prior to the scoring models, approval for financial assistance could take days or weeks. This could hurt the borrower in the case of time-sensitive purchases. Speed has become one of the most significant benefits of using a credit scoring model, as thousands of applications are able to be processed quickly and impartially. It could take as little as a few minutes for a lender to approve decisions for car loans, mortgages, and even things like extended a limit on a current credit card. The data that comes from scoring models also makes financial statements, credit accounts, and credit ratings more accurate even though they can be issued very quickly.

These models also help limit human errors, things that could present serious liabilities in today’s litigious culture. It also reduces the losses a company could experience as a result of bad debt. Without the warnings or red flags that a scoring model issue, businesses may be too hasty in extended credit to unreliable customers. A business is able to specify what information or factors they want to be assessed when processing an application, giving valuable insight as to whether they will be working with a low-risk or high-risk customer. These decisions improve business efficiency and reduce the cost of issuing car loans, credit cards, and mortgages.

CONSUMER BENEFITS OF SCORING MODELS

A consumer is able to obtain much needed financial support when a credit score can be used to demonstrate credit-worthiness. Personal loans can be acquired for a variety of reasons, but a credit score reduces the subjectivity or judgment that had been used in the past to evaluate whether or not a person should be given a chance at credit. The impersonal score, apart from the decisions of the consumer that create the score, makes it much easier for individuals to know their potential when applying for funds. Consumers are also in control of their score, with a higher score and better lending terms being the reward for on-time payments or other responsible payments of any debts. The length of stable credit history also improves a consumer’s potential for gaining access to additional credit lines in the future when the need arises.

It can take a lifetime to build up a high FICO score and only one missed or late payment to ruin it. Whenever you think about your financial situation, always take care to protect your credit score and financial reputation.