Discover essential tips for transitioning from personal money management to achieving business success. Gain insights for effective financial strategies.

Making the leap from personal financial management to steering a business is a pivotal milestone. What got you here won’t get you there. Transforming into an entrepreneurial mindset is crucial. While budgeting and saving have served individuals well, strategic investing now fuels growth. This new world opens up as you shift perspective and add tools to your belt. Although the unknown may be unnerving, the potential rewards justify embracing new skills. This guide illuminates the road ahead, offering practical tips for mastering small business finances.

We’ll unpack everything, from optimizing profits to building your financial network. With an open mind and a commitment to ongoing learning, financial literacy can evolve into a core competitive advantage. Equipped with insight, surround yourself with support, and the path to entrepreneurial prosperity awaits. Let’s get you started on the right foot!

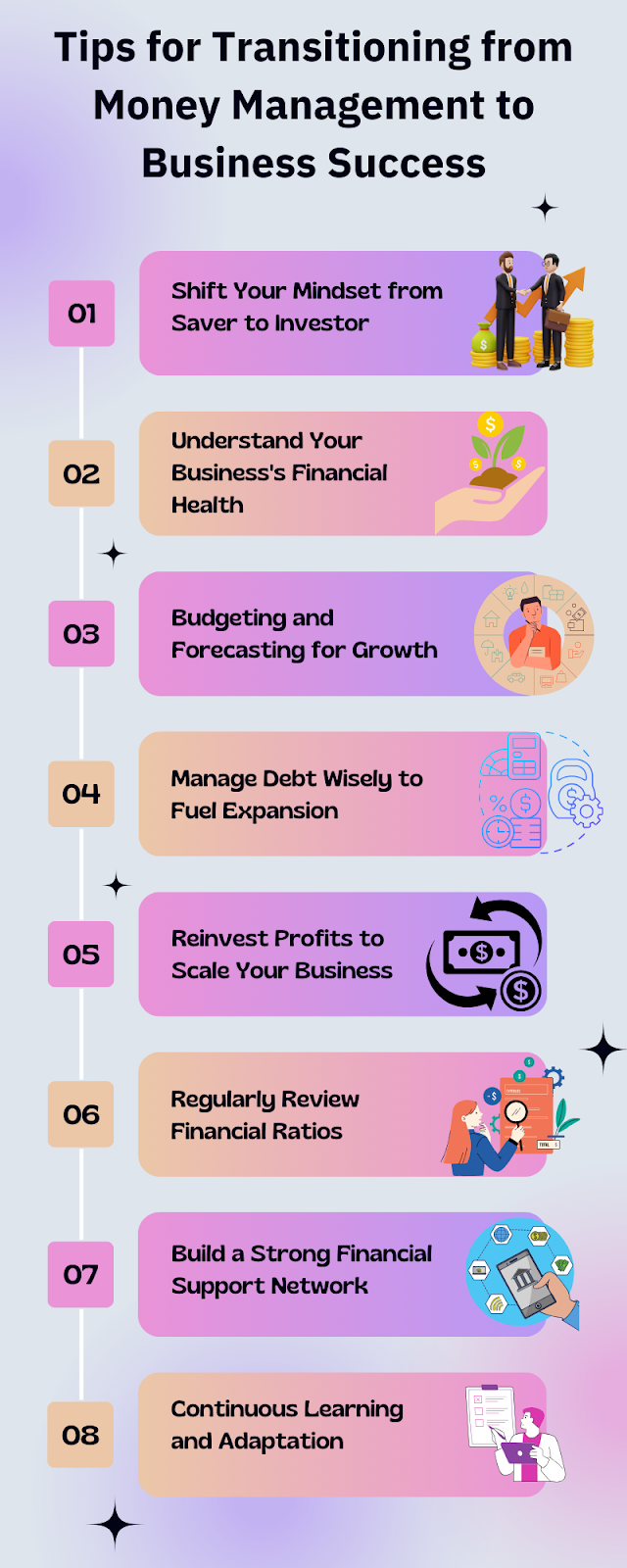

Shift Your Mindset from Saver to Investor

As an entrepreneur, your relationship with money must evolve from accumulator to cultivator. While personal finance focuses on savings and stability, business finance centers on strategic growth through investment. Viewing your finances with an investor mindset unlocks the full potential of your company. Rather than simply preserving capital, identify opportunities to enrich it. Analyze where injecting funds can amplify revenue and profitability down the line. Resist the scarcity instinct to avoid all expenses and instead optimize your resources for calculated returns.

Of course, balance is key—set aside sufficient savings for a rainy day, but funnel excess funds into expansion resources like equipment, employees, facilities, or marketing initiatives. With a sound business model and execution, investing in scalability leads to self-sustaining growth and profitability over time. Make the mental shift from penny-pinching to value creation and watch your business flourish.

Understand Your Business’s Financial Health

Mastering the financial pulse of your business marks a seminal milestone. Just as routine checkups maintain personal health, diagnosing your company’s fiscal condition safeguards success. Start by reviewing key financial statements like your income statement, balance sheet, and cash flow monthly. Look at annual and quarterly patterns. Calculate profitability by product or service line. Tally up debt obligations and terms. Identify your strongest and weakest metrics. Use accrual-based reports in combination with cash-based analytics like bank reconciliations to assess day-to-day liquidity.

Go beyond past performance by forecasting future cash flows and potential vulnerabilities before they arise. Use tools like break-even and working capital analysis to gain practical insights. Schedule regular financial review meetings, much like a doctor’s visit. Knowing your numbers deeply empowers you to make smart management decisions, enrich strengths, and remedy problems, keeping your business healthy and thriving for the long run.

Budgeting and Forecasting for Growth

With a firm grasp on your financial health, the next imperative step is transforming raw numbers into actionable plans. Budgeting and forecasting serve as the yin and yang for optimizing financial management and aligning spending with strategic goals. A budget provides the cornerstones, and forecasting lays the path ahead. Coordinate the two diligently. Build flexibility into your budget categories to adapt to shifting needs, rather than setting rigid limits. Expect revisions as market conditions and operational needs evolve. Allocate budgeted funds across variable operating expenses, fixed overhead, and strategic growth initiatives. Then utilize forecasting tools to translate goals into quantifiable projections.

The model projected sales, costs, cash flows, and KPIs under multiple scenarios: conservative, moderate, and optimistic. Anticipate contingencies like slowed growth or cash shortfalls and have contingency plans ready. Develop resilience by bracing for unanticipated events. With budgeting guiding spending and forecasting mapping the terrain ahead, your fiscal strategy can navigate adversity and capitalize on opportunities.

Manage Debt Wisely to Fuel Expansion

Sometimes, growing your business requires enlisting external capital from lenders. When used strategically and conservatively, debt can serve as rocket fuel to accelerate expansion. The key is balancing the risks with fiscal prudence tailored to your situation. Only pursue debt for driving material business growth, like funding working capital, investing in revenue-boosting capabilities, or smoothing uneven cash flows – not covering basic operating expenses. Seek financing only after exhausting internal capital resources first. Utilize projections to carefully analyze repayment ability before borrowing to avoid overextending.

Different cities have varying levels of business debt burden, with areas like New York, Los Angeles, and Dallas often ranking among the highest. Texas, in particular, has seen a significant rise in business debt levels in recent years, with many companies struggling to maintain a healthy debt-to-capital ratio. A general rule of thumb is to keep your business debt within 30% of your business capital.

Exceeding this number can lower your business’s credit score and give lenders the impression that you are irresponsible with your business’s funds. If you find yourself in a situation where your business debt in Texas has spiraled out of control, Texas debt relief programs can help you get your finances back on track. These programs can help your business thrive again by developing a tailored plan.

Maintaining a healthy debt load is crucial for long-term sustainability and growth potential. Don’t let debt become an albatross; proactively manage it through prudent planning and expert guidance when needed.

Reinvest Profits to Scale Your Business

Scaling your business relies on consistently funneling a portion of profits back into operations for self-sustaining growth. Set aside personal draws temporarily and redirect earnings into enriching capabilities. Analyze higher-margin products and service lines to guide investment. Fund working capital so you can meet demand without cash shortfalls. Upgrade the technology infrastructure to boost productivity. Hire key roles that generate an outsized impact. Enhance facilities as needs evolve.

Expand marketing programs by allocating resources toward the highest ROI channels. Weigh growth prospects against liquidity needs to determine ideal profit reinvestment levels, often 15–25%. Balance growth allocations with emergency reserves and required distributions. Link measurable Key Performance Indicators to capital investments to track returns, demonstrating the wisdom of enriching your capabilities. Establish a regular pattern of wise profit reinvestment to drive a stable expansion, then gradually scale up efforts as justifiable by proven returns.

Regularly Review Financial Ratios

Monitoring raw financial figures provides only part of the fiscal health picture for a small business. Regularly calculating and analyzing key financial ratios every quarter allows a more multidimensional assessment to diagnose strengths to leverage and areas needing improvement from different vantage points. Comparing ratios to internal projections and industry benchmarks also adds context for evaluating status.

Key categories of ratios to focus on include profitability, liquidity, leverage, and efficiency ratios. Profitability ratios like gross profit margin, net profit margin, and return on assets quantify sales and profit levels relative to benchmarks. Liquidity ratios such as the current ratio and cash ratio reveal short-term financial flexibility to cover obligations. Leverage ratios, including debt-to-equity and debt service coverage, compare balance sheet debts against earning ability. Finally, efficiency ratios like inventory turnover and receivables turnover indicate how well systems convert assets into cash flow.

Each ratio formula provides unique diagnostic insight. For example, declining liquidity and leverage ratios over time may signal cash flow and debt difficulties ahead that require intervention, even if profitability appears temporarily unaffected. Reviewing ratios as a whole system flags issues missed when assessing individual reports in isolation.

Enlisting financial partners like accountants, advisors, and business peers to help interpret trends through a ratio analysis lends a broader perspective. Outsider assessments counteract overly optimistic or pessimistic self-appraisals. Use these unbiased insights to fine-tune financial strategy, spending habits, capital allocations, and operations toward ratios aligned with benchmarks and projections.

Making ratio analysis part of quarterly fiscal check-ups spots financial weaknesses early when they are still correctable before cascading into larger issues. Building this diligence safeguards against threats left unseen when only consulting raw figures sporadically. Regular ratio reviews and prudent responses provide a pathway toward sustained stability and growth for small business prosperity.

Financial Ratio: Recommended Ranges

| Ratio | Recommended Range |

| Gross Profit Margin | 35-50% |

| Net Profit Margin | 5-20% |

| Return on Assets | 10-20% |

| Current Ratio | 1.5-3x |

| Cash Ratio | 0.5-1.0x |

| Debt-to-Equity Ratio | 1.0-2.0x |

| Debt Service Coverage | 1.0x or greater |

| Inventory Turnover | 4-8x annually |

| Receivables Turnover | 10-15x annually |

Build a Strong Financial Support Network

Navigating entrepreneurship can be filled with financial unknowns. Cultivating a network of knowledgeable mentors and peers helps shed light and provides accountability. Identify qualified mentors who bring complementary financial acumen and experience to advise you. Their expertise helps guide unfamiliar decisions and spot potential risks. Vet candidates based on merit, not just warm rapport. Fairly compensate advisors for time and effort.

Peer groups enable meaningful exchange and benchmarking. Align with other driven professionals at your stage, pursuing shared success. Attend local meetups or form your own mastermind group. Nurture these relationships through open communication, mutual effort, and tangible gratitude. No entrepreneur is an island. Surrounding yourself with supportive yet objective financial guidance and camaraderie smooths the journey.

Continuous Learning and Adaptation

Mastering business finance is a lifelong endeavor as markets, regulations, and innovations continuously evolve. Committing to regular education in financial management and leadership practices keeps skills sharp and strategies relevant. Read industry-specific publications. Take mini-courses at community colleges. Maintain memberships in professional organizations to stay abreast of trends, best practices, and policy changes.

Study tactics from the world’s most successful modern companies. Absorb wisdom from books by accomplished entrepreneurs. While foundational financial concepts serve as cornerstones, be willing to adapt approaches in response to new technologies and ideas. Listen to feedback from your support network. Keep an open yet shrewdly discerning mindset to weigh innovations thoughtfully. The wisdom to know what to hold onto and when to evolve helps sustain prosperity.

Frequently Asked Questions

- How much of my profits should I reinvest in my business?

Reinvesting 15–25% of profits allows for business growth while still allowing for distributions. Pick a percentage based on the current stage, goals, cash levels, and industry benchmarks. Remain nimble but consistent to instill fiscal discipline.

- When is the right time to seek external financing for business expansion?

Seek financing when current opportunities outweigh debt burdens. First, maximize internal funding and assets. Then analyze growth potential, the ability to repay loans, and overall company financials to determine the ideal timing and payoff.

- How can I manage business finances without a finance background?

Tools like Quickbooks and courses at community colleges build baseline financial skills. Meet with small business counselors for guidance on accounting, reporting, budgeting, and more based on your experience level and business stage. Consider a part-time financial manager.

- What are early signs that my business may be financially unhealthy?

Falling revenue, decreasing margins, lack of profitability, cash flow issues, high debts, and lack of financial planning are red flags. Intervene quickly by controlling costs, securing capital, and optimizing operations through financial analyses.

- Should I produce my financial statements in-house or outsource them to an accountant?

Outsource to an accountant, especially in the early stages, to ensure accurate reporting. As the company grows, consider adding an in-house finance expert to collaborate for ideal insight, tax planning, and trend analysis unique to the business.

- How often should I review my business’s budget?

Review budgets monthly by analyzing variances and adjusting spending accordingly. Re-forecast quarterly based on the latest performance metrics to manage profits and have an up-to-date outlook.

- What is the right cash reserve target for a small business?

Aim for a cash reserve fund equal to 3-6 months of fixed operating expenses. This provides a buffer for managing fluctuations in income and expenses.

- Should I rent or buy when acquiring business real estate?

Review factors like financing terms, ownership tax advantages, expected occupancy timeframe, and local market conditions. Model the total costs of renting vs. buying to determine the more prudent option.

- How do I value my small business for potential sale or transfer?

Business valuation combines weighted factors like cash flow, revenue, profit margins, assets, liabilities, growth rate, trends, and peer comparables. Work with a credentialed valuation expert for an objective appraisal.

- What are the signs that it is time to scale up my staffing levels?

Signals like declining output or quality, missed growth opportunities, employee burnout, payroll fully optimizing your time, and financial health supporting expansion indicate hiring to meet demand may be prudent.

- What financing options exist beyond loans to fund my business?

Equity options like angel investment or private stock can fund growth free of loan constraints. Also consider government grants, partnerships, and revenue-based financing options that link repayment to growth.

Conclusion

Leaping personal finance to business success requires careful planning and execution. As outlined, key tips include developing a business plan, bulking up your savings to handle new expenses, leveraging existing skills, ensuring proper legalities are met, tapping available resources through SBDCs, and approaching new tasks methodically.

The world of entrepreneurship can appear daunting, but with pragmatism, perseverance, and a passion for your venture, prospering is possible. Even if your first endeavor does not reach full success, invaluable experience and knowledge will come from it that will apply to future ideas. Approaching this transition practically while believing in your visions provides the ideal tandem for unlocking your inner business leader.

{kind=link}